Have Stocks & Bond Markets Seen The Lows for This Year?

In short, NO!

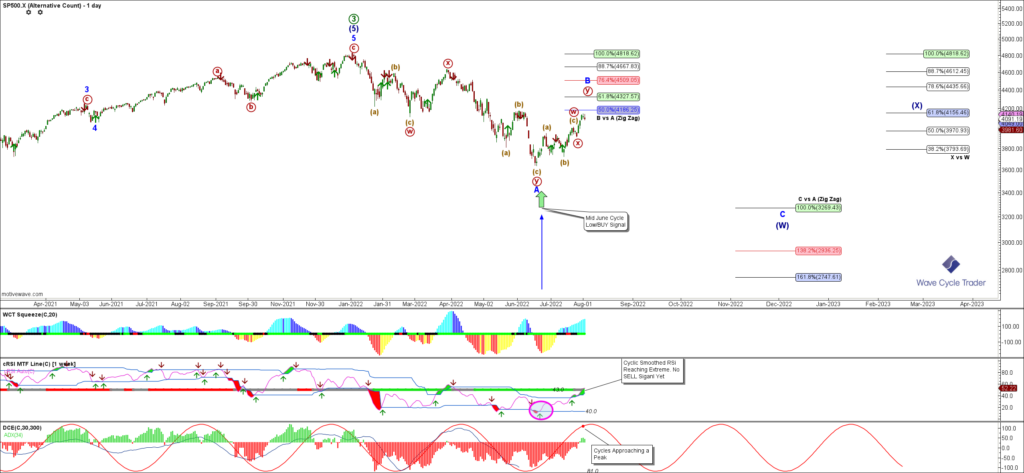

We’ve seen US Stock Indices rally strongly higher off the Mid June 2022 lows in tandem with US Bonds. The conditions were right for this rally, with liquidity being supportive along with the shorter time frame cycles projections we have been posting in the TPA Service suggesting a move up into early to mid August. The Markets did their job of squeezing the shorts and creating a false narrative about pending recession and the end of Fed tightening to drive the rally. It has all been the usual, predicable BS, but it has worked.

So, what can we expect to look forward to from here? With Liquidity now drying up and the shorter time frame cycles starting to point lower and re align with the longer time frame cycles the expectation is for the next leg lower to commence in both equity and bond markets into late November/Late December 2022. This is in line with the long time frame cycles analysis from October 2021.

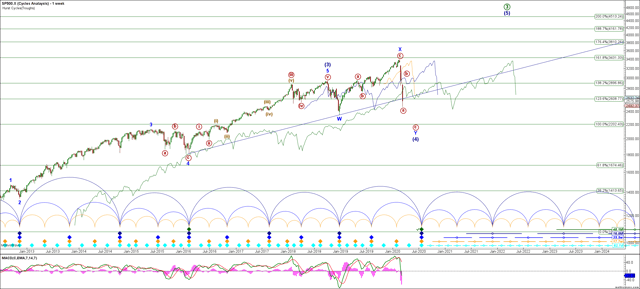

Long Term (Weekly) Cycles:

Looking at the zoomed in current long term weekly cycles, the chart shows that we should still expect further downside into late 2023 to early 2024

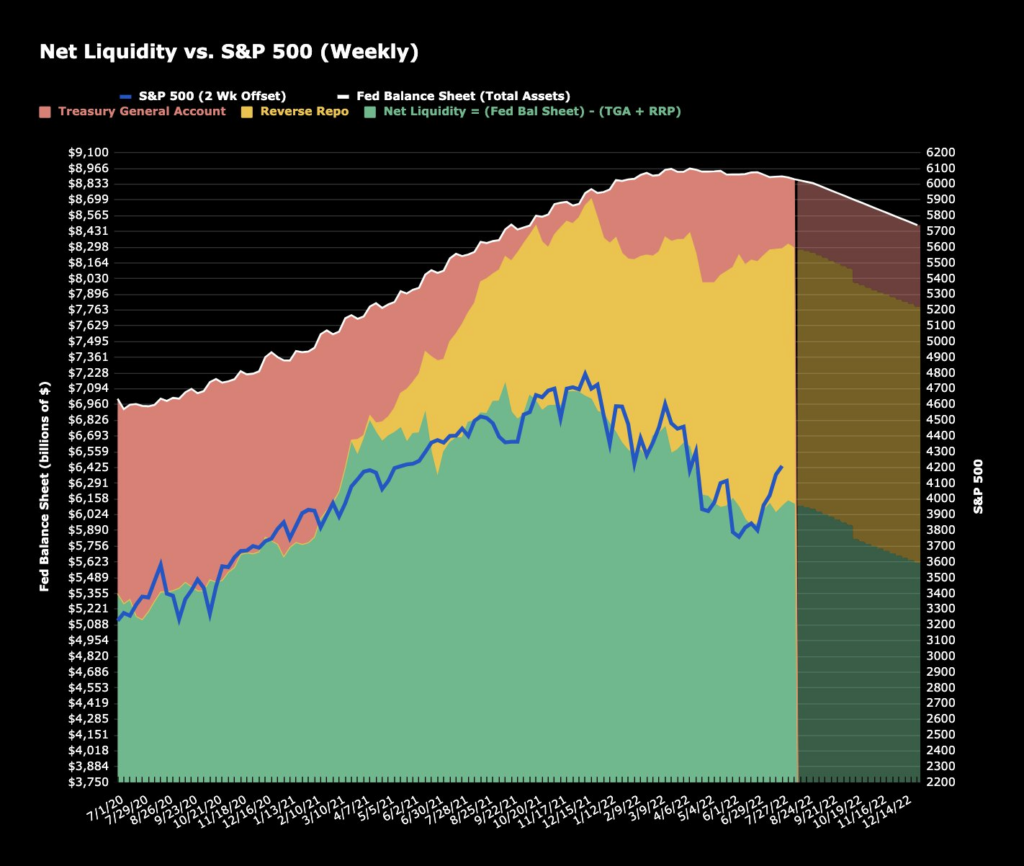

Liquidity:

The US Treasury confirmed yesterday that there will be an enormous increase in supply in August. On July 19, the Treasury started issuing T-bills again. In the last two weeks that issuance has soared to $40 billion per week. We’ve seen Treasury issuance go from a net paydown of $12 billion in the 3 weeks ended July 21 to net issuance of $104 billion this week, with another $40 billion already scheduled for August 9.

The liquidity line stays flat, and Treasury supply crosses above it. The gap will only increase from here as the Fed withdraws cash from dealer and investor accounts, and thereby, the banking system at large.

Furthermore, Treasury supply will only increase. The TBAC Treasury supply forecasts were underestimating forthcoming supply. That’s because, to start with, the May TBAC forecast did not account for QT. Yesterday (August 2) the Treasury confirmed that with the beginning of its releases on the quarterly refunding & that we are headed for a gargantuan increase in supply, beginning now.

The stock and bond rallies are likely to reverse and it is time to be on the look out for the SELL Signals to take advantage of the downside.